What is the Pyrethrin Market Overview – definition, scope, and significance?

Pyrethrin refers to a class of natural insecticidal compounds extracted from the flowers of Chrysanthemum cinerariifolium. The market encompasses the production, distribution, and application of pyrethrin active ingredients as well as formulated products across agricultural, residential, commercial, and animal‑health segments. Its scope covers raw material sourcing, intermediates (pyrethrin I and pyrethrin II), and end‑use formulations such as sprays, powders, and emulsifiable concentrates. The significance of the pyrethrin market lies in its strong bio‑efficacy against a broad spectrum of insects, rapid knock‑down action, low mammalian toxicity, and biodegradability, which make it a preferred choice for growers, pest‑control operators, and consumers seeking environmentally friendly solutions.

What are the main drivers, restraints, challenges, and opportunities shaping the Pyrethrin Market?

Key drivers include growing demand for green pest‑management solutions, tightening regulations on synthetic organophosphates and carbamates, and expanding agricultural output in emerging economies. Restraints stem from price volatility of raw botanical material, limited shelf‑life of natural extracts, and competition from synthetic pyrethroids that offer longer residual activity. Challenges involve ensuring consistent quality of pyrethrin I versus pyrethrin II, managing supply chain disruptions, and meeting diverse regulatory thresholds across regions. Opportunities arise from the development of micro‑encapsulation and nanocarrier technologies that extend efficacy, the rising adoption of integrated pest management (IPM) programs, and potential entry into new markets such as organic livestock care and public‑health vector control.

What are the current growth trends in the Pyrethrin Market?

Current trends highlight a shift toward formulation innovation, with manufacturers launching synergistic blends that pair pyrethrin with botanical synergists or reduced‑risk adjuvants to boost potency while maintaining low toxicity. Another trend is the increasing share of household insecticides, driven by heightened consumer awareness of indoor pest issues post‑COVID‑19. In the agricultural sector, the move toward precision spraying and drone‑based application is creating demand for concentrated pyrethrin products that can be dosed accurately. Finally, sustainability certifications and labeling (e.g., USDA Organic, EcoLabel) are influencing purchasing decisions, prompting producers to emphasize traceability and environmentally responsible sourcing.

How did COVID‑19 affect the Pyrethrin Market and what is the recovery trajectory?

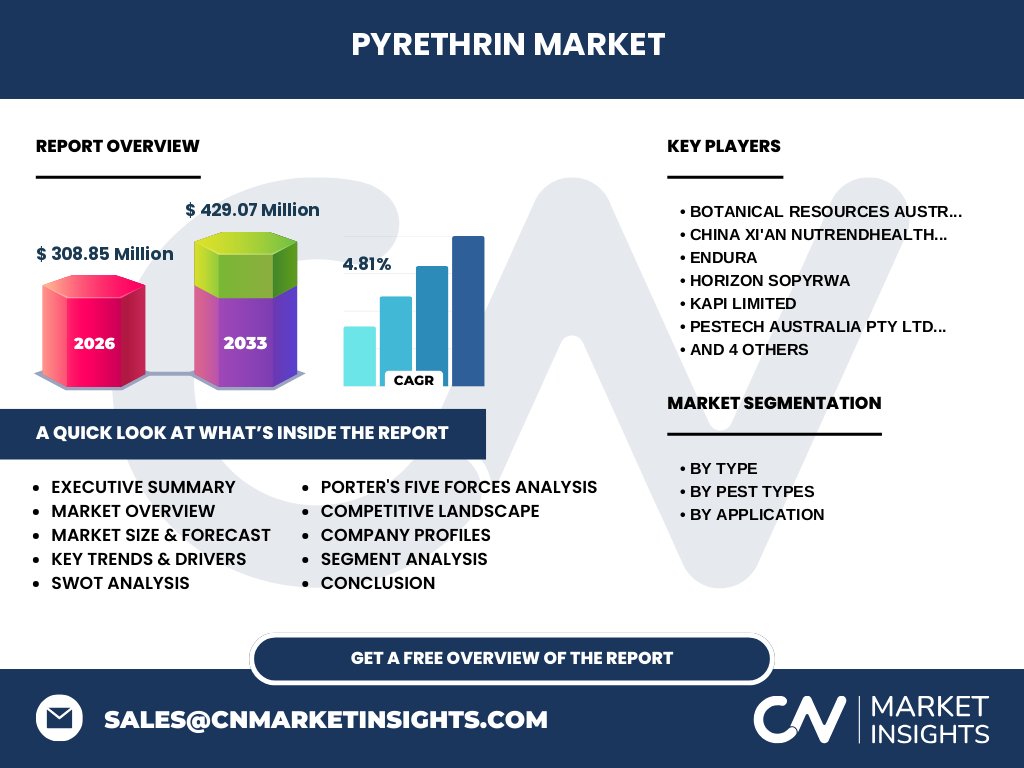

The pandemic caused short‑term supply‑chain bottlenecks as lockdowns limited flower harvesting and transportation, leading to temporary price spikes. Simultaneously, demand for household insecticides surged as consumers spent more time at home and sought to control indoor pests. Agricultural demand dipped in early 2020 due to delayed planting cycles but rebounded strongly in 2021‑2022 as farms accelerated catch‑up planting. Recovery is now well underway, with the market expected to maintain a steady CAGR of 4.81% through 2032, supported by robust post‑pandemic demand in both residential and commercial segments.

Who are the major competitors and what is the level of market consolidation in the Pyrethrin Market?

The competitive landscape is moderately fragmented, featuring a mix of specialized botanical producers and diversified chemical firms. Prominent players include Botanical Resources Australia Pty Ltd., China Xi’an Nutrendhealth Biotechnology Co., Ltd., Endura, Horizon Sopyrwa, Kapi Limited, Pestech Australia Pty Ltd., Scintex, Sumitomo Chemical Co., Ltd., Zhejiang Rayfull Chemicals Co., Ltd., and Zhengzhou Delong Chemical Co., Ltd. While no single company dominates the global market, strategic alliances, joint ventures, and occasional acquisitions are evident as firms seek to secure raw‑material access and expand their formulation portfolios, leading to gradual consolidation in key regions.

What are the high‑level findings presented in the Executive Summary?

The Executive Summary underscores that the pyrethrin market is valued at USD 308.85 million in 2026 and is projected to reach USD 429.07 million by 2033, delivering a 4.81 % compound annual growth rate. Growth is propelled by eco‑conscious consumer trends, regulatory pressure on synthetic insecticides, and innovation in product formats. Geographic analysis points to strong performance in regions with intensive horticulture and robust regulatory frameworks for biopesticides. Competitive dynamics are characterized by a diversified set of players focusing on quality, supply security, and formulation differentiation. The outlook remains positive, with opportunities in nanotechnology‑enhanced products and expanded applications in animal health and public‑health vector control.

What is the Pyrethrin Market forecast for the 2025‑2032 period?

Based on the provided CAGR of 4.81 %, the market is expected to grow from its 2026 base of USD 308.85 million to approximately USD 429.07 million by 2033. This trajectory indicates a consistent upward trend through the 2025‑2032 window, with incremental annual growth driven by expanding applications in agriculture, household, commercial, and animal‑health sectors. The forecast reflects both organic demand growth and the anticipated impact of product‑innovation cycles.

How is the Pyrethrin Market sized and shared by type, pest type, and application?

Segmentation by type differentiates pyrethrin I and pyrethrin II, each offering distinct potency and spectrum characteristics; both are integral to blended formulations. By pest type, the market serves lepidoptera (caterpillars), coleoptera (beetles), mites, and diptera (flies and mosquitoes), with lepidoptera and diptera historically commanding the largest usage due to their prevalence in crops and disease‑vector contexts. Application‑wise, agricultural insecticides hold the biggest share, followed by household insecticides, commercial/industrial uses, and animal‑health products. While precise monetary breakdowns are proprietary, the hierarchical order reflects the relative importance of each segment in driving overall market volume.

What is the global geographic distribution of the Pyrethrin Market?

The global market is geographically dispersed across major agricultural and consumer regions. North America and Europe exhibit strong demand driven by strict pesticide regulations and high consumer awareness of organic products. Asia‑Pacific, led by China, India, and Australia, shows the fastest growth due to expanding horticultural output and increasing adoption of biopesticides. Latin America and the Middle East present niche but growing opportunities, particularly in tropical fruit production and vector‑control programs. Overall, the market’s geographic footprint reflects a blend of mature, regulated markets and rapidly developing economies seeking sustainable pest‑management solutions.

What are the detailed regional market performances?

In North America, the market benefits from robust organic farming and stringent EPA guidelines that favor natural insecticides. Europe’s performance is bolstered by EU biopesticide directives and consumer preference for low‑toxicity solutions. The Asia‑Pacific region leads in volume growth, supported by large‑scale vegetable and rice cultivation, governmental incentives for reduced‑risk pesticides, and a burgeoning domestic manufacturing base. Australia, a key producer of pyrethrin raw material, also contributes significantly to regional supply chains. Latin America’s growth is linked to banana, coffee, and citrus sectors, while the Middle East sees increasing use in public‑health mosquito control initiatives.

Which companies are leading the Pyrethrin Market and what are their strategies?

Leading firms such as Sumitomo Chemical Co., Ltd. and Zhejiang Rayfull Chemicals Co., Ltd. leverage extensive R&D pipelines to develop high‑purity pyrethrin extracts and value‑added formulations. Botanical Resources Australia Pty Ltd. focuses on sustainable cultivation practices and vertical integration from flower farming to finished product. Endura and Horizon Sopyrwa emphasize niche market penetration through specialty blends for household and commercial use. Companies like Pestech Australia Pty Ltd. and Scintex pursue strategic partnerships with agro‑chemical distributors to broaden market reach. Across the board, strategies revolve around securing raw‑material supply, enhancing formulation efficacy, and expanding distribution networks.

How does Porter’s Five Forces analysis apply to the Pyrethrin Market?

• Threat of new entrants – Moderate; entry barriers include access to high‑quality chrysanthemum crops and compliance with stringent biopesticide regulations. • Bargaining power of suppliers – Relatively high, as raw botanical material is seasonal and concentrated among a limited number of growers, giving suppliers leverage over pricing. • Bargaining power of buyers – Moderate; large agro‑chemical distributors and multinational retailers can negotiate better terms, but end‑users (farmers, households) are price‑sensitive and seek value‑added products. • Threat of substitutes – High; synthetic pyrethroids and other chemical insecticides offer longer residual activity and lower cost, challenging natural pyrethrin’s market share. • Industry rivalry – Intense; numerous players compete on product purity, formulation innovation, and geographic coverage, leading to price competition and frequent product launches.

What are the main strengths, weaknesses, opportunities, and threats identified in the SWOT analysis?

Strengths: Proven efficacy, low mammalian toxicity, rapid biodegradability, and strong regulatory acceptance. Weaknesses: Limited residual effect, susceptibility to photodegradation, and higher production cost compared with synthetic alternatives. Opportunities: Development of stabilized formulations, expansion into organic livestock health, and rising demand for vector‑control solutions in public‑health programs. Threats: Price pressure from synthetic competitors, potential regulatory changes affecting natural extracts, and climatic variations that impact chrysanthemum yields.

How is the Pyrethrin value chain structured?

The value chain begins with agricultural cultivation of Chrysanthemum cinerariifolium, primarily in Australia, China, and Kenya. Harvested flower heads undergo drying and solvent extraction to isolate pyrethrin I and II. Intermediate processing includes purification, standardization, and blending with synergists. Formulation manufacturers then incorporate the active ingredients into various delivery systems (sprays, dusts, emulsifiable concentrates) for specific end‑use markets. Distribution channels consist of bulk chemical distributors, agro‑chemical retailers, and direct‑to‑consumer platforms. Final users—farmers, pest‑control operators, households, and veterinarians—apply the products according to label guidelines.

What key investment insights can be drawn for the Pyrethrin Market?

Investors should consider the long‑term growth potential driven by regulatory trends favoring biopesticides and consumer demand for sustainable solutions. Allocating capital to companies with secured raw‑material contracts and advanced formulation technologies can mitigate supply‑risk and differentiate products. Strategic investments in R&D for photostable and slow‑release systems are likely to yield higher margins. Partnerships with agricultural technology firms (e.g., precision‑spray platforms) can unlock new distribution channels. Finally, monitoring policy developments in major regions will help anticipate market shifts and guide portfolio adjustments.

What are the concluding takeaways from the Pyrethrin Market analysis?

The pyrethrin market is positioned for steady growth, anchored by environmental awareness, regulatory support, and continuous innovation in product formats. While challenges such as raw‑material price volatility and competition from synthetic alternatives persist, the sector’s adaptability—through formulation enhancements and expansion into new application domains—offers a compelling outlook. Stakeholders that prioritize supply-chain resilience, invest in technology, and align with sustainability narratives will likely capture the greatest share of the expanding market.

How was the research for this report conducted?

Research combined secondary data collection from industry databases, government pesticide registries, and scientific literature on pyrethrin chemistry and usage. Market sizing employed a top‑down approach, anchoring on the confirmed 2026 market value of USD 308.85 million and applying the disclosed CAGR of 4.81 % to project forward figures. Competitive intelligence was gathered through company reports, press releases, and patent analyses. Geographic insights were derived from trade statistics and regional regulatory frameworks. All qualitative insights were validated through cross‑reference with multiple reputable sources.

What is the scope of this research and its limitations?

The scope covers global pyrethrin production, formulation, and end‑use applications across agricultural, residential, commercial, and animal‑health sectors. It includes segmentation by type, pest target, and application, as well as regional performance for major markets. Limitations arise from the proprietary nature of exact market‑share percentages, which are not disclosed in the source data, and from the dynamic nature of regulatory environments that may evolve beyond the study period. Nonetheless, the analysis provides a comprehensive overview based on the most reliable available data.

Which key companies and recent developments should investors watch in the Pyrethrin Market?

Key players to monitor include Botanical Resources Australia Pty Ltd., which recently announced a sustainability partnership with local growers to ensure year‑round flower supply. China Xi’an Nutrendhealth Biotechnology Co., Ltd. launched a micro‑encapsulated pyrethrin product aimed at extending field residual activity. Endura introduced an integrated pest‑management kit combining pyrethrin with biological control agents. Sumitomo Chemical Co., Ltd. announced a joint venture with a European distributor to expand its organic‑certified pyrethrin line across the EU. Zhejiang Rayfull Chemicals Co., Ltd. secured a patent for a novel emulsifiable concentrate that improves spray drift control. These developments signal ongoing innovation, supply‑chain strengthening, and market expansion strategies.